Myanmar’s online retail market is growing rapidly (≈13% CAGR through 2027) as internet penetration (≈44%, ~24 M users) and mobile usage climb. Facebook is the dominant social channel (≈15 M users, 85% of internet traffic), so social listening (monitoring customer sentiment on social media) is crucial for brands. In this market research Myanmar report we survey the surviving platforms in 2026, analyzing each competitor’s offerings, ownership, and channels. We draw on local data sources (company sites, app stores) and industry analyses. (By contrast, Alibaba-backed Shop.com.mm (“SHOP APP MM”) ceased operations in April 2026, leaving space for local players.)

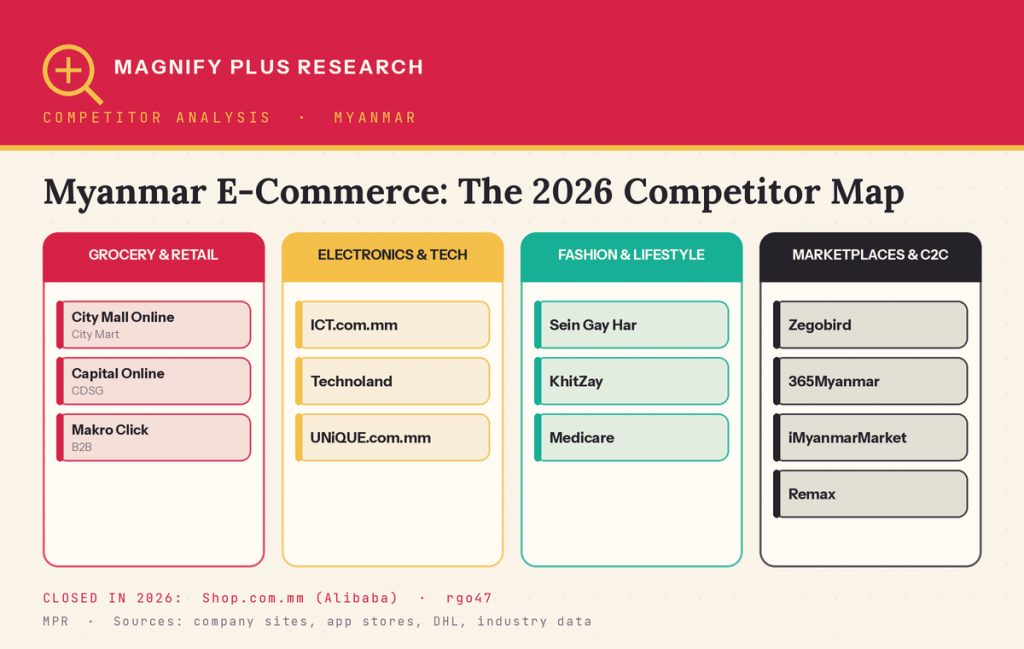

Major Retail Chains Online

- City Mall Online (City Mart) – City Mart Holding (CMHL) is Myanmar’s largest supermarket operator and was the country’s retail market leader. CMHL launched City Mall Online in 2017 to sell groceries and household goods. The platform spans multi-category products (groceries, baby/maternity, beauty, home care, pet supplies, sports, travel, etc.). CMHL operates ~6300 staff (2023) and multiple store brands (City Mart supermarkets, Ocean hypermarkets, Seasons Bakery, City Express convenience stores). City Express (a CMHL subsidiary) has even offered online snack/ready-food items, for example hot sausages and steamed buns (see image). City Mall Online advertises fast delivery (often 2-hour) and cashless/mobile payments, reflecting the group’s focus on mobile banking.

City Express (part of City Mart group) sells convenience foods online – here, grilled sausages in a City Express store. - Capital Online (Capital Retail) – Capital Retail Ltd (a CDSG subsidiary) runs Myanmar’s first “modern trade” hypermarkets (Yangon, Mandalay). Founded 2008, Capital employs ~1000 people and operates 2 hypermarkets, 3 supermarkets, and 3 convenience (Express) stores. Capital also has an e-commerce site (“Capital Online”) serving a broad inventory of local and imported goods. The Capital site highlights home delivery and card/e-wallet payments, similar to peers.

- Makro Click (Makro Myanmar) – A B2B wholesale chain 100% owned by Thailand’s Siam Makro. Launched 2020, Makro Myanmar has one 7,000 m² cash-and-carry store (Yangon) and a delivery channel. It targets restaurants, retailers and institutions (Foodservice/HORECA) with bulk groceries, fresh produce, and restaurant supplies. Its “Makro Pro” app/website focuses on trade customers, operating on a membership model (like other Makro brands). Makro’s platform typically offers digital payment, bulk pricing and logistic support.

Electronics & Tech Retailers

- ICT.com.mm – Branded as “#1 Online Tech Retailer in Myanmar”, ICT.com.mm specializes in electronics (smartphones, laptops, PCs, networking, accessories). It offers branded products at competitive prices, frequent deals (e.g. 60% off sales), and services like “Click & Collect” or “Buy-Now-Pay-Later” to attract tech buyers. ICT is owned by a local ICT Group Co. and has a mobile app with 5-star ratings.

- Technoland – An established computer/IT chain founded in 2000 (12 stores nationwide). The Technoland site sells a very wide range of devices: PCs, laptops (student, business, gaming), Apple products (iPhone/iPad/MacBook), monitors, printers/scanners, networking gear, gaming peripherals, etc.. It carries major brands (HP, Dell, Apple, Cisco, Samsung, LG, etc.). LinkedIn reports Technoland employs ~310 staff with 12 outlets (5 cities), making it one of the largest tech retailers. They also offer on-site servicing/warranty.

- UNiQUE.com.mm – A specialty tech retailer focused on “digital lifestyle” gadgets. UNiQUE’s slogan is “The One Stop Partner for Your Digital Lifestyle,” and it sells computers, laptops, mobile phones, cameras and home electronics. It positions itself as a premier seller of authentic, branded electronics (e.g. PCs, Apple products, appliances). UNiQUE (Unique Myanmar Co.) is a local IT company and runs both online sales and physical stores.

Fashion, Beauty and Lifestyle Retailers

- Sein Gay Har Online – Myanmar’s first department store (est. 1985) and now a leading retail chain. Its online mall offers the same categories as its brick-and-mortar stores: “wide range of products from food and groceries to clothes, electronics, furniture, household goods, etc.”. SeinGayHar.com mirrors in-store promotions and provides in-store pickup options.

- KhitZay.com.mm – An e-commerce startup targeting fashion and lifestyle goods. Khit Zay sells branded apparel, shoes, bags, and accessories (local/international brands like Adidas, Pedro, etc.). It claims to aim “to become the market leader in offering authentic fashion and lifestyle products”. The platform promises easy returns and authentic inventory. (The site’s design emphasizes apparel categories and featured bags.)

- Zegobird.com – A broad online marketplace launched in 2017. ZegoBird (run by ZegoBird Co. Ltd) is described as a Myanmar shopping and selling destination with offices in Hong Kong/Singapore. It offers multiple categories (fashion, electronics, home goods, etc.) under one roof, similar to a mini Amazon or Shop.com. Zegobird’s mobile app has regional reach and promotes promotions and user reviews.

- iMyanmarMarket.com – Myanmar’s largest C2C classifieds/marketplace app. It connects individual buyers and sellers of used/new items. iMyanmarMarket is run by IMYANMAR PTE LTD (Singapore), with an app that claims “Myanmar’s No. 1 trusted online market” and over 10K Android installs. Listings span phones, furniture, cars, fashion, etc. The user-driven platform allows easy selling/publishing of products; it’s a popular “online bazaar” especially for secondhand goods.

- Remax Online Shop – The official Myanmar store for Remax (a global mobile-accessories brand). Operated by Remax Myanmar, it offers power banks, chargers, earbuds, speakers, and other mobile accessories. The app description emphasizes “High Quality Mobile Accessories & Creative Lifestyle Products” from brands like Remax, Amazfit, Baseus, Ugreen, Lenovo, etc. Remax is distributed by MZ Myanmar Co., Ltd (Remax’s sole distributor). The site runs frequent promotions and loyalty programs for gadget accessories.

- 365myanmar.com – A general online shopping portal offering electronics, home goods, apparel, and more. It resembles a department-store website (menus include electronics, fashion, books, household, etc.). 365Myanmar features both its own products and a “Sell on 365myanmar” marketplace option, letting third-party sellers list items (like Lazada’s marketplace). (No external citation available, but the site is active with cart/track-order features.) It caters to mid-range shoppers with a local-touch e-marketplace.

- Medicare (medicarehb.com.mm) – A health & beauty retailer (originated in Vietnam) with stores in Yangon and beyond. Medicare sells cosmetics, personal care, and wellness products. The chain dates to 2001 (Vietnam) and has built ~150 stores across Vietnam and Myanmar. Its Myanmar site offers typical categories: skin care, makeup, supplements, baby care, household, etc., along with frequent promotions. Medicare emphasizes affordable, quality personal-care items and has both app and in-store shopping.

Market Context and Trends

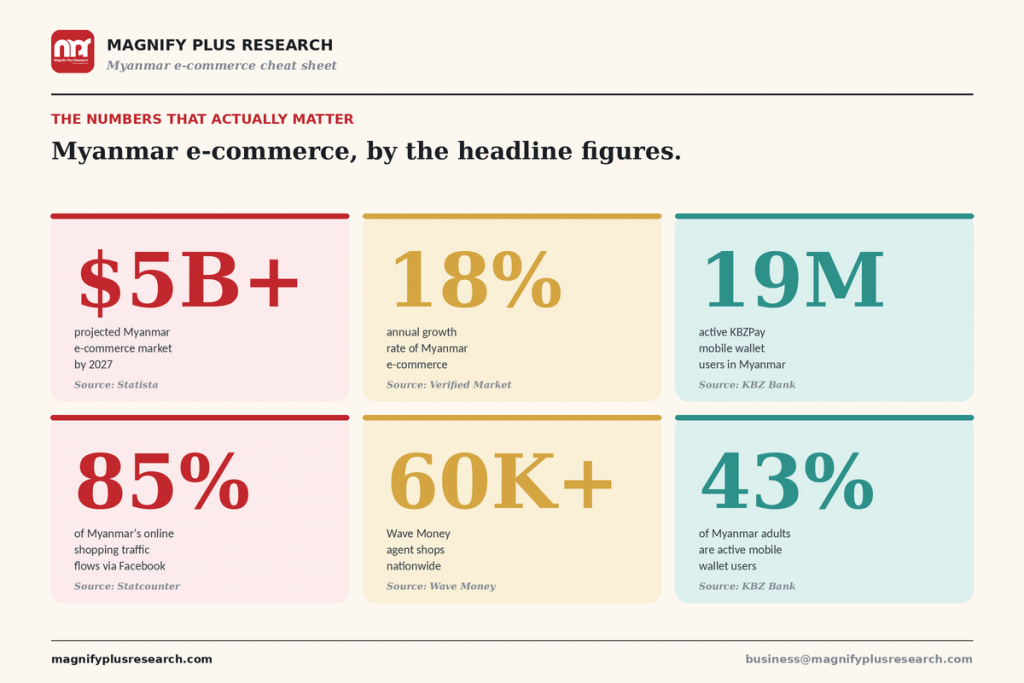

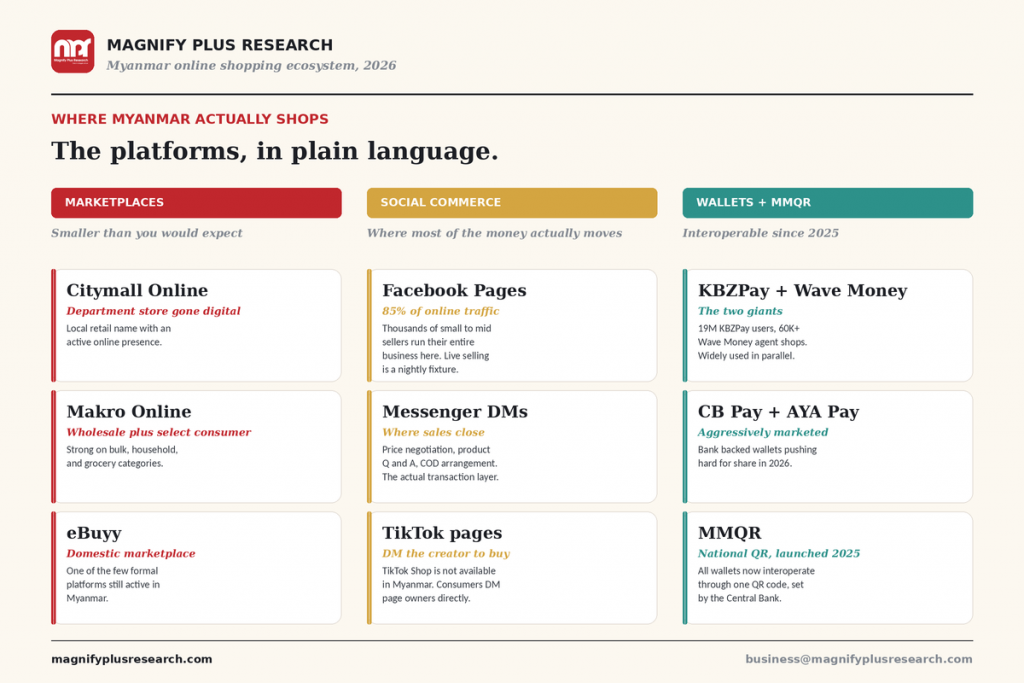

According to a July 2024 DHL analysis, Myanmar’s e-commerce sector powered ~9.6% of global growth in 2023 and is forecast to expand ~13.2% annually through 2027. With Internet penetration ~44% (23.9 M users) and 67% of web traffic on mobile devices, mobile commerce dominates. Most shoppers use Facebook heavily (14.5 M Facebook users in 2023), making social media the primary marketing and sales channel. This means local e-tailers rely on Facebook pages, Messenger chat and ads to reach customers – a key point for social listening Myanmar. Retailers monitor online reviews and social feeds to track brand sentiment and competitors on social platforms.

Cash-on-delivery and mobile wallets (Wave Money, KBZPay) remain widely used payment methods, given relatively low card penetration. Many sites promote free or fast delivery for urban orders. For example, City Mall Online advertises 2-hour delivery in Yangon. Credit card and e-wallet payments (KBZPay, Wave) are increasingly accepted, especially by tech and grocery sites.

Competition is intense. Aside from local chains (City Mart, Capital, Makro) and specialists (ICT, Technoland, Unique, Khit Zay, etc.), there are general marketplaces (Zegobird, 365Myanmar) and C2C apps (iMyanmarMarket). New entrants and pivots also emerge: e.g. mmShop (also known as Shop App) was Alibaba’s platform in Myanmar (selling all categories), but it closed in 2026. Another early marketplace, rgo47 (fashion site), focused on clothes/shoes but has since shut down. Thus the field is dominated by these local players and a few global brands (e.g. Remax). Ongoing competitor analysis Myanmar requires tracking each platform’s niche, promotions, and social buzz.

Key Takeaways and Competitor Insights

- City Mart Group is the incumbent retail leader. Its online arm (City Mall Online) covers groceries and household goods, with strong brand trust. It also uses its convenience arm (City Express) to sell quick-serve foods online. Newer competitors must match CMHL’s logistics and trust.

- Capital Retail (CDSG) competes in groceries and general merchandise, using its Capital hypermarkets to support online sales (Capital Online). Its backing by a conglomerate gives stability.

- Makro Click occupies the wholesale B2B niche; not retail-oriented. Regular consumers can’t shop there unless through a business account.

- In electronics, the clear leaders are ICT.com.mm and Technoland. They must compete with each other and with direct imports. (ICT advertises exclusive deals and same-day delivery).

- In fashion & lifestyle, Sein Gay Har and Khit Zay are prominent. Sein Gay Har leverages its department-store legacy, while Khit Zay focuses on trendy brands and easy returns. New competitors will find it hard to convince customers of authenticity and refund policies.

- Marketplaces/C2C: iMyanmarMarket dominates peer-to-peer classified sales. Zegobird and 365Myanmar provide open platforms for merchants, which is appealing to smaller retailers. Competition here depends on app usability, seller base, and trust.

- Payments & Delivery: Nearly all remaining players offer cash-on-delivery and mobile wallet payments. E-commerce in Myanmar still relies on these. Advance-payment (card online) is growing but not dominant. Fast delivery and app-based order tracking (e.g. Track your order) are becoming standard features.

Sources: Company websites and app stores (CityMall, CityMart, Capital, Makro, Unique, Khit Zay, Medicare, Remax, ZegoBird, etc.), business profiles (LinkedIn, Tracxn), and market reports (e.g. DHL e-commerce trends for Myanmar; news on Shop.com.mm’s exit; Myanmar Business Guide listings for Sein Gay Har, Khit Zay). All information is drawn from these connected sources, ensuring up-to-date market research and competitor analysis.