We’ve always believed the same thing about market research: the technology and the data matter, but the value comes from what a capable team does with them. The best decisions in Myanmar aren’t made by the companies with the most data — they’re made by the ones who turn that data into clear, confident action. That’s why we’re introducing MPR Professional Services: a set of capabilities designed to help your team get more out of every study, every dataset, and every decision.

Why we built it

Working with brands across Myanmar, we kept seeing the same pattern. The organisations getting the most from research weren’t necessarily the biggest spenders — they were the ones with the right support at the right moments: help executing studies cleanly under pressure, and a strategic partner to connect the findings to the decisions that actually mattered.

But not every team has the time or in-house bandwidth to do both well. Fieldwork is demanding, timelines are tight, and the leap from “we have the data” to “we know what to do” is exactly where good intentions stall. MPR Professional Services exists to close that gap — to put our experience to work as an extension of your team.

Two ways we support you

MPR Professional Services is built on two pillars: Project Services and Strategic Services.

Project Services — an extra set of expert hands

When your team is stretched and the deadline is real, we take the load. Project Services make sure your research is set up well and delivered cleanly, so you can focus on the decisions rather than the logistics.

Study design and setup — We partner with you to scope the study, design the questionnaire, and configure fieldwork so it answers the real question, not an approximate one. (Disciplined questionnaire design — keeping studies tight and respondent-friendly — is something we hold a hard line on.)

Fieldwork execution and quality control — Our field network and QC processes handle the hard part of Myanmar research: reaching the right respondents and standing behind the data.

Analysis and reporting — We turn raw data into clear, decision-ready findings, so the insight arrives usable rather than as a spreadsheet to wrestle.

Strategic Services — connecting insight to impact

Individual studies are useful. Connected insight is transformative. Strategic Services help you move from collecting data to building a genuine, compounding understanding of your market.

Strategic consultancy — Experienced researchers work with you to make sure every study ties back to a real business objective and a real decision.

Connected learnings — By reading patterns across multiple studies and waves, we surface the bigger picture that single projects miss.

Local-language and listening expertise — Burmese-language analysis and social listening, validated by people who actually understand the market, layered into your strategic picture.

Set up to get it right from the start

A recurring frustration we hear is teams feeling they never quite got their research function set up properly. So Professional Services includes a structured onboarding: we help you get questionnaire frameworks, reporting structures, audience definitions and benchmarks right from day one, so the value compounds instead of being rebuilt each time.

For teams that want more, we offer tailored add-ons — bespoke study designs for unusual research needs, custom benchmarking against the right competitive set, and specific audience builds so your insight comes from exactly the consumers who matter to you.

Why it matters

This isn’t about selling extra services. It’s about making sure your investment in research actually moves the business. Every study you commission should bring you closer to a sharper strategy, a stronger campaign, or a better-informed decision. MPR Professional Services is how we make that more reliable — by giving your team time back, or by sharpening the strategic value of what you already have.

Insight shouldn’t be a bottleneck. It should be the thing that gives you the edge in a market most competitors are still guessing at. We’d love to show you what that looks like for your team.

Frequently asked questions

What is MPR Professional Services? A set of capabilities — Project Services and Strategic Services — designed to help teams get more value from their research, whether that’s extra hands to execute studies or strategic guidance to connect insight to decisions.

Who is it for? Brands and teams operating in Myanmar that want to run high-quality research without the full in-house burden, or that have data and want help turning it into strategy.

How is this different from a standard research project? A standard project delivers a study. Professional Services wraps that in support — from setup and quality control through to cross-study strategic interpretation — so research becomes a compounding asset rather than a series of one-offs.

Can you support ongoing programmes, not just one-off studies? Yes. Strategic Services are built for continuity — brand tracking, connected learnings across waves, and programme management for more complex insights needs.

Let’s talk: Want to see what MPR Professional Services could do for your team? Get in touch →

For a few weeks every four years, football reorganises daily life in Myanmar. Sleep schedules bend around late-night kickoffs, tea shops fill past midnight, and a country with deep football roots tunes in to the biggest sporting event on earth. With the 2026 World Cup now underway, there’s a window of intense, emotional, shareable attention — and most brands miss it, because they’re looking in the wrong place. The action isn’t only on the pitch or the broadcast. It’s in the network of group chats, fan pages and tea-shop tables where Myanmar actually experiences the tournament.

Football is already woven into Myanmar life

Start with how deep this runs. Southeast Asia is one of football’s most passionate regions — a majority of football supporters here follow the English Premier League, and broadcasters across the region carry all 380 matches a season despite most games airing in the middle of the night (SPORTFIVE). Myanmar fits that pattern: European club football, ASEAN competitions, and above all the World Cup command real, committed audiences. This isn’t casual interest a brand has to manufacture. It’s existing passion a brand can join — if it shows up authentically.

The hidden network: where Myanmar actually watches

The most important shift for marketers is that the fan conversation has gone semi-private and mobile. In Myanmar, watching the World Cup is rarely a solo, single-screen activity. It happens:

In tea shops and homes, often communally, late into the night.

On a second screen — fans follow the match while simultaneously reacting, joking and arguing on their phones. Sports consumption here is phone-led: people track scores, clips and commentary on the move, in tea shops, on the bus, during breaks (mobile-first sports consumption in Myanmar).

Inside Facebook groups, Messenger threads, Viber and Telegram chats — the Myanmar equivalent of the private fan communities reshaping World Cup conversation worldwide. This is where reactions spread, memes circulate, and the real emotional life of the tournament happens.

The lesson mirrors what’s been observed globally: the second screen has become the primary engagement layer, especially for younger fans. But in Myanmar the network runs on Facebook, Messenger, Viber and Telegram rather than WhatsApp — a crucial localisation that off-the-shelf global playbooks get wrong.

Why this matters: the commercial opportunity

A captive, emotional, highly engaged audience for a few concentrated weeks is rare. The World Cup delivers exactly that in Myanmar — and the brands that benefit aren’t necessarily the official sponsors. They’re the ones who understand fan behaviour well enough to show up in the right place, in the right tone, at the right moment.

Real-time and reactive beats polished

Football moments are unpredictable and intensely shareable — a stunning goal, an upset, a controversial call. Content that reacts fast, in an authentic, low-polish way, travels far through group chats; glossy, slow, pre-approved campaigns don’t. Speed and relatability outperform production value during a tournament.

Meet the late-night, mobile reality

Kickoffs land late and viewing is mobile and communal. Activations, offers and content should fit that rhythm — built for a phone, timed to the match, designed to be forwarded.

Respect the spaces fans own

The private group chat is the fan’s space, not the brand’s billboard. Brands earn a place there by being genuinely useful or genuinely funny — not by intruding. Forwardable content that fans choose to share is the goal.

What research reveals that observation can’t

You can see that Myanmar loves football. What you can’t see by watching is which teams and players dominate Myanmar conversation, how sentiment swings across the tournament, what fans actually say in Burmese, and which brand moments land versus fall flat. That’s where Burmese-language social listening and survey work come in — turning visible passion into specific, usable insight about your category and your audience.

[MPR DATA → insert findings from any World Cup or football fan study you’ve run: dominant teams/players in Myanmar conversation, sentiment patterns, fan demographics, second-screen behaviour, what fans respond to. This is your chance to own a topical, highly shareable data story — and it pairs naturally with our Mobile Legends gaming research as proof of capability.]

The bottom line

The World Cup is one of the few moments when a whole market leans in at once — and in Myanmar, the real tournament happens as much in tea shops and group chats as on the broadcast. Brands that understand that hidden network, move at its speed, and ground their approach in real fan data don’t interrupt the moment. They become part of it.

Frequently asked questions

How popular is the World Cup and football in Myanmar? Very. Football is deeply embedded in Myanmar life, with strong followings for the World Cup, European club football (especially the Premier League), and ASEAN competitions — consistent with Southeast Asia’s status as one of football’s most passionate regions.

Where do Myanmar fans engage during the World Cup? On a phone-led second screen and in semi-private communities — Facebook groups, Messenger, Viber and Telegram — alongside communal viewing in tea shops and homes, often late at night to match European and tournament kickoff times.

What kind of World Cup content works in Myanmar? Fast, authentic, low-polish, forwardable content that reacts to real match moments and fits a mobile, late-night, communal viewing pattern — generally outperforming slow, glossy campaigns.

How can brands measure football fan behaviour in Myanmar? Through Burmese-language social listening and survey research, which reveal which teams and players dominate conversation, how sentiment shifts, and what fans actually respond to.

About the author: [BYLINE PLACEHOLDER — Name, role, credential line, headshot, LinkedIn.]

Sources: SPORTFIVE (Premier League in Southeast Asia); mobile-first sports consumption in Myanmar; DataReportal Digital 2026 Myanmar. The 2026 FIFA World Cup runs from June to July 2026 — confirm tournament dates and update topical references at publication.

Every major decision a brand makes in Myanmar rests on data it cannot personally verify. You didn’t knock on the doors or make the calls — you’re trusting that someone did, properly, and reported it honestly. That trust is the entire product of a research firm. And in an era when a convincing-looking chart can be generated in seconds, knowing whether to trust the number behind it has never mattered more. This article is about how to tell trustworthy research from the kind that just looks trustworthy.

Why trust is the real deliverable

Strip away the decks and dashboards and what a research firm actually sells is confidence — the right to act on a number without re-checking it yourself. If that confidence is misplaced, everything built on top of it is too: the budget, the launch, the market-entry decision. In Myanmar the stakes are higher than usual, because there’s little public data to cross-check against. When the research is the only window onto the market, the integrity of that window is non-negotiable.

The AI-era risk: data that looks right but isn’t

It has never been easier to produce numbers that look authoritative. Synthetic charts, plausible-sounding percentages, AI-summarised “findings” with no fieldwork underneath — all of it can be generated fast and presented cleanly. The danger isn’t that this data is obviously fake; it’s that it’s superficially convincing and quietly hollow. For a market research firm, fabricated or unverifiable numbers aren’t a shortcut — they’re a fatal credibility risk, because the moment a client catches one, every other number is suspect too. The defence is the same as it’s always been, just more important now: real fieldwork, transparent method, and honest limitations.

How to tell trustworthy research from the rest

Here’s what to look for — and what should make you pause.

Transparent methodology

Trustworthy research shows its working. You should be able to see the method (face-to-face, telephone, online, qualitative), the sample size, the geography, the fieldwork dates, and how the data was weighted. Red flag: a confident headline with no methodology section, or a vague one you can’t interrogate.

Honest sampling and coverage

A credible partner tells you exactly who was and wasn’t reached — including the regions a Myanmar sample couldn’t cover this wave. Red flag: national claims with no detail on regional coverage, or an online sample presented as if it represents the whole country.

Real first-party fieldwork

The strongest signal of all is primary data the firm actually collected, with the method to prove it. Red flag: secondary statistics recycled from the internet and dressed up as original insight.

Stated limitations

Counter-intuitively, a report that admits what it can’t tell you is more trustworthy than one that claims certainty about everything. Red flag: no caveats at all. In a market as complex as Myanmar, that’s not confidence — it’s a tell.

Traceable sources

Every external figure should trace back to a named, primary source you can check. Red flag: numbers with no provenance, or citations that lead nowhere.

Trust is harder — and more valuable — in Myanmar

Two local realities raise the bar. First, the scarcity of public data means you often can’t fact-check a finding against an independent source, so the firm’s own integrity carries more weight. Second, the operating environment is genuinely difficult — access varies, conditions change — which makes it tempting for less scrupulous providers to paper over gaps rather than disclose them. The firms worth trusting do the opposite: they’re most transparent precisely where the data is hardest to get. That candour is the signal. (It’s also why we’re explicit about method throughout our guide to market research in Myanmar.)

How we earn it

We’d rather tell you what we don’t know than pretend to certainty we haven’t earned. In practice that means every study states its method and sample plainly; first-party data is labelled as such, and external figures are sourced and linked; coverage limits are disclosed wave by wave; and Burmese-language analysis — in surveys and social listening alike — is validated by people, not just models. [MPR DATA → insert your specific quality-control and validation steps, e.g. back-checking, interviewer audits, dual-coding.] None of this is glamorous. It’s just what makes a number worth acting on.

The bottom line

Anyone can produce a confident chart. The question that matters is whether there’s real, honestly-reported fieldwork underneath it. In Myanmar, where you often can’t check the market yourself, that’s not a technicality — it’s the whole basis on which you’re betting your budget. Trust isn’t a soft value in research. It’s the product.

Frequently asked questions

How do I know if market research data is trustworthy? Look for transparent methodology (method, sample size, geography, dates, weighting), honest coverage disclosure, genuine first-party fieldwork, stated limitations, and traceable sources. Absence of these is the warning sign.

Why is data integrity a bigger issue now? Because convincing-looking numbers and AI-generated summaries are easy to produce without any real fieldwork behind them. The risk isn’t obvious fakery — it’s polished data that’s quietly hollow.

Why is trustworthy research especially important in Myanmar? Public data is scarce, so you often can’t independently verify findings. That puts more weight on the research firm’s own integrity and transparency.

Is AI bad for market research? Not inherently — used well, it speeds up analysis. The danger is using it to manufacture findings without real data. The safeguard is human-validated fieldwork and transparent method.

About the author: [BYLINE PLACEHOLDER — Name, role, credential line, headshot, LinkedIn.]

Work with a firm that shows its working:Talk to MPR →

“Should we do qualitative or quantitative research?” is one of the most common questions we hear — and it’s usually the wrong question. The better one is: what decision are you trying to make? Qualitative and quantitative research answer fundamentally different questions, and choosing well in a market as challenging as Myanmar can be the difference between insight you can act on and an expensive shrug. This guide explains what each method does, when to use which, and how to combine them.

The core difference, in one line

Quantitative research tells you how many and how much; qualitative research tells you why and how. One measures, the other explains. A survey can tell you that 40% of consumers switched to a cheaper brand last quarter; only a focus group or in-depth interview will tell you the reasoning, emotion and context behind that switch. You usually need both eventually — but rarely at the same moment.

Quantitative research: measuring the market

Quantitative research produces numbers you can project, compare and track — market sizes, awareness levels, usage rates, preference scores. In Myanmar it’s delivered mainly through:

Face-to-face surveys (CAPI) — the most representative method, because it reaches the large offline population.

Telephone surveys (CATI) — fast and broad, ideal for tracking and quick-turn questions.

Online surveys — economical and quick, but skewed toward a younger, more urban audience.

Use quantitative when you need to: size an opportunity, measure awareness or brand health, test concepts at scale, segment the market, or track change over time. If the question starts with “how many,” “what share,” or “how has it changed,” it’s a quantitative job.

Qualitative research: understanding the why

Qualitative research trades breadth for depth. Instead of many people answering fixed questions, a smaller number explore a topic in their own words. In Myanmar it usually means:

Focus group discussions (FGDs) — guided group conversations that surface shared attitudes, language and reactions.

In-depth interviews (IDIs) — one-on-one conversations for sensitive topics or detailed individual journeys.

Use qualitative when you need to: understand motivations, explore how people talk about a category, react to early ideas, diagnose a problem a survey flagged, or develop hypotheses before measuring them. If the question starts with “why,” “how,” or “what would happen if,” it’s a qualitative job.

In Myanmar, qualitative work is also where local moderation matters most. Nuance in Burmese, regional dialect and social context simply don’t survive a translated guide run by an outsider — a point worth weighing heavily when choosing a partner.

When to use which: a simple decision guide

You need a number to put in a plan or report → quantitative.

You need to understand a behaviour or attitude → qualitative.

You have a surprising survey result and don’t know why → qualitative follow-up.

You have a strong hunch and need to confirm it at scale → quantitative.

You’re developing something new from scratch → qualitative first, then quantitative to validate.

The real answer: combine them

In practice, the strongest research programmes use both in sequence. A common and powerful pattern: qualitative to explore, quantitative to measure, qualitative to explain. Explore a new category with focus groups to learn the language and the landscape; run a survey to size and quantify what you found; then return to qualitative to interpret the surprising numbers. Each method covers the other’s blind spot.

Social listening adds a valuable third layer here — the unprompted, real-time voice of the market — but it complements rather than replaces structured qualitative and quantitative work. For the full picture of methods and trade-offs in this market, see our guide to market research in Myanmar.

The bottom line

Don’t start by choosing a method. Start by naming the decision. Once you know whether you need to measure something or understand it, the choice between quantitative and qualitative makes itself — and in a market as nuanced as Myanmar, knowing which question you’re really asking is half the value.

Frequently asked questions

What’s the difference between qualitative and quantitative research? Quantitative research measures — how many, how much, what share — using surveys with larger samples. Qualitative research explains — why and how — using focus groups and in-depth interviews with smaller numbers of people.

Which should I use for my project? It depends on your decision. Use quantitative to measure, size, or track; use qualitative to understand motivations, explore ideas, or diagnose a problem. Many projects benefit from both in sequence.

Is qualitative research reliable if it uses so few people? Yes, for its purpose. Qualitative research isn’t meant to be statistically representative — it’s meant to explain and explore in depth. Use quantitative research when you need projectable numbers.

Why does local moderation matter in Myanmar? Because Burmese nuance, dialect and social context are easily lost in translation. Qualitative research run by people who understand the local culture produces far richer, more accurate insight.

About the author: [BYLINE PLACEHOLDER — Name, role, credential line, headshot, LinkedIn.]

Most companies operating in Myanmar don’t have a data shortage — they have a decision shortage. Numbers sit in a deck, a quarter goes by, and the sales and marketing teams keep targeting on instinct. The value of market research isn’t the report; it’s the decisions the report makes possible. This article is about closing that gap: turning consumer and market data into the targeting, segmentation, and go-to-market moves that actually grow revenue in Myanmar.

From data to decisions: what “decision-grade” really means

Plenty of data is technically accurate and practically useless — too old, too vague, or too disconnected from a decision anyone is about to make. Decision-grade data is different. It’s current, it’s specific to the choice in front of you, and it points to an action. In a market like Myanmar, where conditions shift quickly and official statistics are thin, the half-life of insight is short. Data that was decision-grade six months ago may simply be wrong today.

The practical test we apply: can a sales or marketing leader do something differently because of this number? If not, it’s trivia, however precise. Everything below is about producing data that passes that test.

One clear view of the market you’re actually selling to

The first job is a single, honest picture of demand — who buys, where, how much, and why. In Myanmar that picture has to be built from primary fieldwork rather than pulled off a shelf, because the shelf is mostly empty. Done right, it answers the questions sales and marketing keep guessing at:

Who is the real buyer? Not a borrowed regional persona, but the actual Myanmar consumer or business, segmented by geography, age, income band, and behaviour.

Where is the demand concentrated? Yangon, Mandalay, and other centres behave very differently; a single national average hides the map you need.

What drives the choice? Price, trust, availability, social proof — the weighting varies by category and changes under economic pressure.

[MPR DATA → insert an example of a demand profile you built for a client and the decision it sharpened.]

Align effort with opportunity, not instinct

The most common waste in Myanmar go-to-market isn’t bad targeting — it’s untargeted effort spread evenly across a market that is anything but even. Research lets you concentrate. Three moves consistently pay off:

Size the opportunity before you chase it

Market sizing and segment-level demand estimation tell you which segments and regions are worth the cost of pursuit and which aren’t. Effort follows opportunity instead of habit.

Define an ideal customer profile that fits Myanmar

A profile imported from another market quietly mis-aims your whole funnel. A locally built ICP — grounded in who actually converts here — focuses acquisition spend where return is highest.

Prioritise channels by where your buyers really are

In Myanmar that increasingly means a Facebook- and Messenger-led path to discovery and purchase, alongside traditional trade. Channel strategy should follow the evidence, not the org chart. (Our consumer trends overview covers the behavioural picture.)

Engage with context, not guesswork

Once you know who and where, research sharpens how. The difference between a message that lands and one that’s ignored is usually context: the right language (literally — Burmese nuance matters), the right value framing for a price-sensitive moment, the right proof points for a market that runs on trust and word of mouth. Concept testing, message testing, and qualitative work let you pressure-test creative and positioning before you spend media against it — which in a tight market is the difference between budget invested and budget burned.

Keep the data alive

Decision-grade data isn’t a one-off purchase; it’s a maintained asset. Markets move, and a profile that’s never refreshed decays into the same stale assumptions research was meant to replace. The teams that win here treat insight as a running capability — periodic tracking, refreshed segmentation, a feedback loop between what marketing ships and what the market does. That’s also where brand health tracking and ongoing listening earn their place: they keep the picture current between big studies.

The bottom line

Data only creates value at the moment it changes a decision. In Myanmar — opaque, fast-moving, and easy to misread — the brands that turn research into specific, current, locally-grounded moves on targeting, segmentation, and messaging don’t just market more confidently. They spend less to sell more. That’s the whole point of getting the data right.

Frequently asked questions

What is “market research data” used for in sales and marketing? To target the right customers, size and prioritise opportunities, build an accurate ideal customer profile, choose the right channels, and test messaging before spending media — turning guesswork into grounded decisions.

Why can’t I just use regional data for Myanmar? Because Myanmar behaves differently from neighbours that look similar, and its demand is highly uneven by region and segment. Imported benchmarks mis-aim targeting and messaging. Local, primary data is what makes the difference.

How current does market data need to be? Current enough to reflect today’s conditions. In a fast-moving market like Myanmar, insight has a short shelf life, so the most valuable data is regularly refreshed rather than bought once.

How do I make research actionable rather than just interesting? Tie every study to a specific decision a sales or marketing leader is about to make. If a finding can’t change an action, it isn’t decision-grade.

About the author: [BYLINE PLACEHOLDER — Name, role, credential line, headshot, LinkedIn.]

A brand is not just a product. It is the symbol customers attach their trust to, and in a competitive market that trust is one of the most valuable assets a business owns. So when a company decides to change its name, reposition, or rebrand, it is not simply swapping out a logo. It is moving the thing customers have quietly decided to rely on.

Get it right, and a rebrand refreshes the business and opens the door to new audiences. Get it wrong, and years of hard-won loyalty can walk out with the old name. The difference between those two outcomes usually comes down to a single question that too many businesses skip: how will our customers actually feel about this change?

That is a question you can answer before you commit, not after. This is exactly what consumer perception research is built to do, and it is one of the most valuable applications of market research in Myanmar today.

Why rebranding is riskier than it looks

Aggressive marketing has turned brands into genuine assets. A name carries associations built over years: reliability, familiarity, a sense of who the company is and who it is for. When that name changes, all of those associations are suddenly up for renegotiation in the customer’s mind.

The risk is that customers do not experience a rebrand the way the business does. Inside the company, a name change is the end of a long strategic process. To the customer, it can feel abrupt, even suspicious. People wonder what else is changing. They ask whether ownership has changed, whether service quality will slip, whether the thing they trusted still exists under the new name. Left unanswered, those questions turn into hesitation, and hesitation is how loyal customers become switchers.

The uncomfortable reality is that a name change can move brand trust sharply. In illustrative perception studies, the share of customers who describe a brand as trustworthy can fall significantly between the current name and a proposed new one, even when the product, the people, and the service behind it are completely unchanged. Same company, different name, very different level of confidence.

That gap is not a reason to avoid rebranding. It is a reason to measure it first.

What consumer perception research actually measures

Understanding how customers will respond to a rebrand means looking at the complete customer journey, not just a single reaction to a new logo. A thorough study traces every meaningful interaction, from the first moment someone browses or considers the brand, through purchase, activation, and everyday use, all the way to the decisions where a customer chooses to stay or switch.

It also covers the places where those interactions happen. Customers form impressions across retail outlets and online platforms alike, and a perception study that only looks at one channel gives you half the picture. Mapping both ensures the findings reflect how people really experience the brand.

To make sense of all this, our research uses the Pillars of Customer Experience Framework, which isolates the factors that shape how customers perceive a brand. Three of those pillars consistently emerge as the strongest drivers of loyalty and advocacy:

Personalization. Whether customers feel the brand understands and speaks to them specifically.

Integrity. Whether the brand is seen as honest and dependable, which is the pillar most directly threatened by a name change.

Time and effort. Whether dealing with the brand feels easy, or whether every interaction costs the customer something.

By measuring perception against these pillars, a study does more than tell you whether customers like a new name. It tells you why they feel the way they do, and which levers you can pull to protect loyalty through the transition.

The questions a rebranding study should answer

A perception study earns its place by answering the specific questions that determine whether a rebrand succeeds. A well-designed research programme sets out to do the following.

Evaluate customer experience. Apply the Pillars of Customer Experience Framework to assess how personalization, integrity, and time and effort influence customer loyalty and advocacy for your brand.

Analyse market trends. Provide insight into the wider market landscape, including major players and their competitive positioning, so a rebrand is read in context rather than in isolation.

Understand the impact on brand loyalty. Surface the specific concerns and expectations customers hold about a name change, and how those feelings are likely to shift perception once the change goes live.

Identify concerns and expectations. Get to the heart of what customers actually worry about when they hear a brand is changing its name, from fears about service quality to questions about ownership.

Develop consumer personas. Break perception down by demographic so strategy can be tailored to the segments that matter, rather than built on a single average customer who does not exist.

Evaluate communication strategies. Test the most effective ways to announce and explain the change so the business can minimise negative perception and carry existing loyalty into the new identity.

Answer those six questions and a rebrand stops being a leap of faith. It becomes a managed decision with the risks understood and the messaging planned.

Why this matters most in a tough economy

Brand health is easy to take for granted when times are good. It becomes critical when they are not. In a challenging economic climate, customers are more cautious, more price-sensitive, and quicker to reconsider the brands they use. A rebrand introduced without understanding perception can tip already-hesitant customers toward a competitor at exactly the moment a business can least afford to lose them.

This is where research pays for itself. A perception study replaces assumption with evidence, giving decision-makers a clear read on the risk before any money is spent on the rebrand itself. It supports the kind of strategic decision-making that drives growth and builds resilience, rather than gambling equity on a name that looks good in a boardroom but has never been tested with the people who actually pay for it.

If you are considering a rebrand, a repositioning, or a name change of any kind, the single most valuable thing you can do is find out how your customers will react before you act. Perception can be measured. Loyalty can be protected. And the risk of a name change can be turned into a number you can plan around.

Know the number before you make the call.

Frequently Asked Questions

What is consumer perception research?

Consumer perception research measures how customers think and feel about a brand: how much they trust it, how satisfied they are, and how likely they are to stay loyal or recommend it. In a rebranding context, it compares perception of the current brand with perception of a proposed new name, so a business can see the likely impact of a change before committing to it.

How does rebranding affect customer trust?

A name change can significantly reduce customer trust, even when the product and service stay the same, because customers associate the existing name with reliability and familiarity. A new name raises questions about whether ownership, quality, or the brand itself has changed. Research measures the size of that trust shift so businesses can address concerns before they cost them loyalty.

Why should a company do market research before rebranding?

Rebranding puts years of accumulated brand equity at risk. Market research before a rebrand replaces guesswork with evidence, revealing how customers will react, what concerns they hold, and how best to communicate the change. This lets a business make the decision on data rather than on a hunch, and plan messaging that protects existing loyalty.

What is the Pillars of Customer Experience Framework?

It is a framework that identifies the key factors shaping how customers perceive a brand. In perception studies, personalization, integrity, and time and effort consistently emerge as the strongest drivers of customer loyalty and advocacy. Measuring perception against these pillars shows not just whether customers respond well to a change, but why, and which levers protect loyalty.

Does Magnify Plus Research offer rebranding perception studies in Myanmar?

Yes. Magnify Plus Research provides brand and rebranding perception research as part of its market research services in Myanmar, covering the full customer journey across retail and online channels, with consumer personas broken down by demographic and guidance on communicating a change effectively.

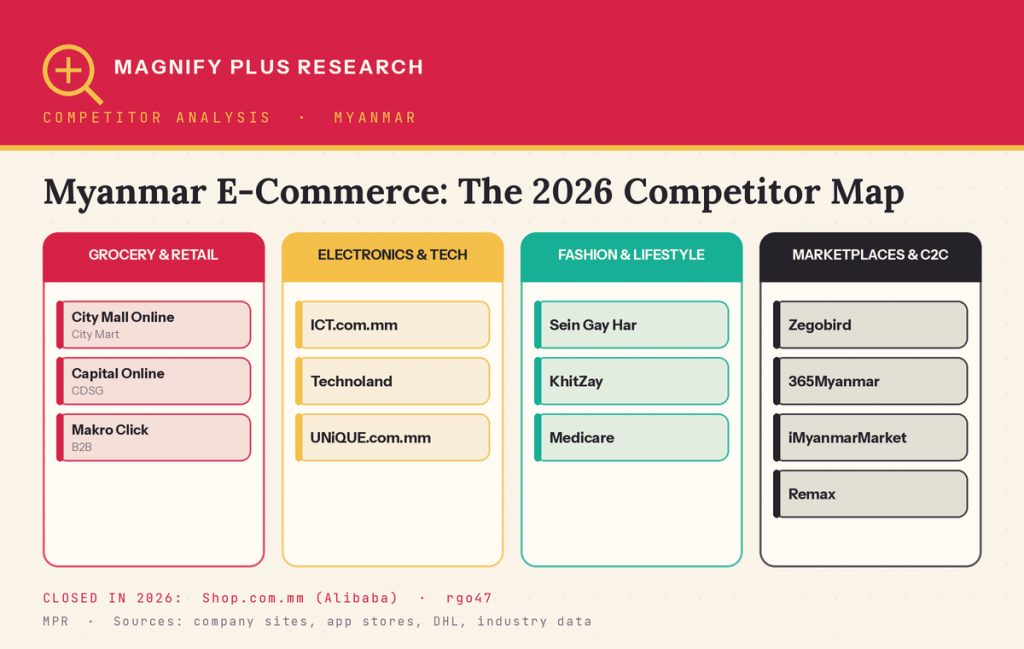

Myanmar’s online retail market is growing rapidly (≈13% CAGR through 2027) as internet penetration (≈44%, ~24 M users) and mobile usage climb. Facebook is the dominant social channel (≈15 M users, 85% of internet traffic), so social listening (monitoring customer sentiment on social media) is crucial for brands. In this market research Myanmar report we survey the surviving platforms in 2026, analyzing each competitor’s offerings, ownership, and channels. We draw on local data sources (company sites, app stores) and industry analyses. (By contrast, Alibaba-backed Shop.com.mm (“SHOP APP MM”) ceased operations in April 2026, leaving space for local players.)

Major Retail Chains Online

City Mall Online (City Mart) – City Mart Holding (CMHL) is Myanmar’s largest supermarket operator and was the country’s retail market leader. CMHL launched City Mall Online in 2017 to sell groceries and household goods. The platform spans multi-category products (groceries, baby/maternity, beauty, home care, pet supplies, sports, travel, etc.). CMHL operates ~6300 staff (2023) and multiple store brands (City Mart supermarkets, Ocean hypermarkets, Seasons Bakery, City Express convenience stores). City Express (a CMHL subsidiary) has even offered online snack/ready-food items, for example hot sausages and steamed buns (see image). City Mall Online advertises fast delivery (often 2-hour) and cashless/mobile payments, reflecting the group’s focus on mobile banking. City Express (part of City Mart group) sells convenience foods online – here, grilled sausages in a City Express store.

Capital Online (Capital Retail) – Capital Retail Ltd (a CDSG subsidiary) runs Myanmar’s first “modern trade” hypermarkets (Yangon, Mandalay). Founded 2008, Capital employs ~1000 people and operates 2 hypermarkets, 3 supermarkets, and 3 convenience (Express) stores. Capital also has an e-commerce site (“Capital Online”) serving a broad inventory of local and imported goods. The Capital site highlights home delivery and card/e-wallet payments, similar to peers.

Makro Click (Makro Myanmar) – A B2B wholesale chain 100% owned by Thailand’s Siam Makro. Launched 2020, Makro Myanmar has one 7,000 m² cash-and-carry store (Yangon) and a delivery channel. It targets restaurants, retailers and institutions (Foodservice/HORECA) with bulk groceries, fresh produce, and restaurant supplies. Its “Makro Pro” app/website focuses on trade customers, operating on a membership model (like other Makro brands). Makro’s platform typically offers digital payment, bulk pricing and logistic support.

Electronics & Tech Retailers

ICT.com.mm – Branded as “#1 Online Tech Retailer in Myanmar”, ICT.com.mm specializes in electronics (smartphones, laptops, PCs, networking, accessories). It offers branded products at competitive prices, frequent deals (e.g. 60% off sales), and services like “Click & Collect” or “Buy-Now-Pay-Later” to attract tech buyers. ICT is owned by a local ICT Group Co. and has a mobile app with 5-star ratings.

Technoland – An established computer/IT chain founded in 2000 (12 stores nationwide). The Technoland site sells a very wide range of devices: PCs, laptops (student, business, gaming), Apple products (iPhone/iPad/MacBook), monitors, printers/scanners, networking gear, gaming peripherals, etc.. It carries major brands (HP, Dell, Apple, Cisco, Samsung, LG, etc.). LinkedIn reports Technoland employs ~310 staff with 12 outlets (5 cities), making it one of the largest tech retailers. They also offer on-site servicing/warranty.

UNiQUE.com.mm – A specialty tech retailer focused on “digital lifestyle” gadgets. UNiQUE’s slogan is “The One Stop Partner for Your Digital Lifestyle,” and it sells computers, laptops, mobile phones, cameras and home electronics. It positions itself as a premier seller of authentic, branded electronics (e.g. PCs, Apple products, appliances). UNiQUE (Unique Myanmar Co.) is a local IT company and runs both online sales and physical stores.

Fashion, Beauty and Lifestyle Retailers

Sein Gay Har Online – Myanmar’s first department store (est. 1985) and now a leading retail chain. Its online mall offers the same categories as its brick-and-mortar stores: “wide range of products from food and groceries to clothes, electronics, furniture, household goods, etc.”. SeinGayHar.com mirrors in-store promotions and provides in-store pickup options.

KhitZay.com.mm – An e-commerce startup targeting fashion and lifestyle goods. Khit Zay sells branded apparel, shoes, bags, and accessories (local/international brands like Adidas, Pedro, etc.). It claims to aim “to become the market leader in offering authentic fashion and lifestyle products”. The platform promises easy returns and authentic inventory. (The site’s design emphasizes apparel categories and featured bags.)

Zegobird.com – A broad online marketplace launched in 2017. ZegoBird (run by ZegoBird Co. Ltd) is described as a Myanmar shopping and selling destination with offices in Hong Kong/Singapore. It offers multiple categories (fashion, electronics, home goods, etc.) under one roof, similar to a mini Amazon or Shop.com. Zegobird’s mobile app has regional reach and promotes promotions and user reviews.

iMyanmarMarket.com – Myanmar’s largest C2C classifieds/marketplace app. It connects individual buyers and sellers of used/new items. iMyanmarMarket is run by IMYANMAR PTE LTD (Singapore), with an app that claims “Myanmar’s No. 1 trusted online market” and over 10K Android installs. Listings span phones, furniture, cars, fashion, etc. The user-driven platform allows easy selling/publishing of products; it’s a popular “online bazaar” especially for secondhand goods.

Remax Online Shop – The official Myanmar store for Remax (a global mobile-accessories brand). Operated by Remax Myanmar, it offers power banks, chargers, earbuds, speakers, and other mobile accessories. The app description emphasizes “High Quality Mobile Accessories & Creative Lifestyle Products” from brands like Remax, Amazfit, Baseus, Ugreen, Lenovo, etc. Remax is distributed by MZ Myanmar Co., Ltd (Remax’s sole distributor). The site runs frequent promotions and loyalty programs for gadget accessories.

365myanmar.com – A general online shopping portal offering electronics, home goods, apparel, and more. It resembles a department-store website (menus include electronics, fashion, books, household, etc.). 365Myanmar features both its own products and a “Sell on 365myanmar” marketplace option, letting third-party sellers list items (like Lazada’s marketplace). (No external citation available, but the site is active with cart/track-order features.) It caters to mid-range shoppers with a local-touch e-marketplace.

Medicare (medicarehb.com.mm) – A health & beauty retailer (originated in Vietnam) with stores in Yangon and beyond. Medicare sells cosmetics, personal care, and wellness products. The chain dates to 2001 (Vietnam) and has built ~150 stores across Vietnam and Myanmar. Its Myanmar site offers typical categories: skin care, makeup, supplements, baby care, household, etc., along with frequent promotions. Medicare emphasizes affordable, quality personal-care items and has both app and in-store shopping.

Market Context and Trends

According to a July 2024 DHL analysis, Myanmar’s e-commerce sector powered ~9.6% of global growth in 2023 and is forecast to expand ~13.2% annually through 2027. With Internet penetration ~44% (23.9 M users) and 67% of web traffic on mobile devices, mobile commerce dominates. Most shoppers use Facebook heavily (14.5 M Facebook users in 2023), making social media the primary marketing and sales channel. This means local e-tailers rely on Facebook pages, Messenger chat and ads to reach customers – a key point for social listening Myanmar. Retailers monitor online reviews and social feeds to track brand sentiment and competitors on social platforms.

Cash-on-delivery and mobile wallets (Wave Money, KBZPay) remain widely used payment methods, given relatively low card penetration. Many sites promote free or fast delivery for urban orders. For example, City Mall Online advertises 2-hour delivery in Yangon. Credit card and e-wallet payments (KBZPay, Wave) are increasingly accepted, especially by tech and grocery sites.

Competition is intense. Aside from local chains (City Mart, Capital, Makro) and specialists (ICT, Technoland, Unique, Khit Zay, etc.), there are general marketplaces (Zegobird, 365Myanmar) and C2C apps (iMyanmarMarket). New entrants and pivots also emerge: e.g. mmShop (also known as Shop App) was Alibaba’s platform in Myanmar (selling all categories), but it closed in 2026. Another early marketplace, rgo47 (fashion site), focused on clothes/shoes but has since shut down. Thus the field is dominated by these local players and a few global brands (e.g. Remax). Ongoing competitor analysis Myanmar requires tracking each platform’s niche, promotions, and social buzz.

Key Takeaways and Competitor Insights

City Mart Group is the incumbent retail leader. Its online arm (City Mall Online) covers groceries and household goods, with strong brand trust. It also uses its convenience arm (City Express) to sell quick-serve foods online. Newer competitors must match CMHL’s logistics and trust.

Capital Retail (CDSG) competes in groceries and general merchandise, using its Capital hypermarkets to support online sales (Capital Online). Its backing by a conglomerate gives stability.

Makro Click occupies the wholesale B2B niche; not retail-oriented. Regular consumers can’t shop there unless through a business account.

In electronics, the clear leaders are ICT.com.mm and Technoland. They must compete with each other and with direct imports. (ICT advertises exclusive deals and same-day delivery).

In fashion & lifestyle, Sein Gay Har and Khit Zay are prominent. Sein Gay Har leverages its department-store legacy, while Khit Zay focuses on trendy brands and easy returns. New competitors will find it hard to convince customers of authenticity and refund policies.

Marketplaces/C2C: iMyanmarMarket dominates peer-to-peer classified sales. Zegobird and 365Myanmar provide open platforms for merchants, which is appealing to smaller retailers. Competition here depends on app usability, seller base, and trust.

Payments & Delivery: Nearly all remaining players offer cash-on-delivery and mobile wallet payments. E-commerce in Myanmar still relies on these. Advance-payment (card online) is growing but not dominant. Fast delivery and app-based order tracking (e.g. Track your order) are becoming standard features.

Sources: Company websites and app stores (CityMall, CityMart, Capital, Makro, Unique, Khit Zay, Medicare, Remax, ZegoBird, etc.), business profiles (LinkedIn, Tracxn), and market reports (e.g. DHL e-commerce trends for Myanmar; news on Shop.com.mm’s exit; Myanmar Business Guide listings for Sein Gay Har, Khit Zay). All information is drawn from these connected sources, ensuring up-to-date market research and competitor analysis.

In April 2026, one of the biggest names in Myanmar online shopping quietly switched off the lights. Shop.com.mm, the Alibaba-backed platform once expected to dominate, closed its doors. When a giant leaves, everyone else inherits its customers, and the scramble to win them is exactly the kind of moment where market research earns its keep.

So who is actually left standing? And more importantly, who is winning? We went through the surviving players, category by category, to map Myanmar’s e-commerce landscape as it looks in 2026. Consider this your field guide to the competition: the incumbents, the specialists, the marketplaces, and the quiet operators most rankings miss.

The state of play: Myanmar e-commerce in 2026

Before we meet the contenders, a quick lay of the land, because the rules of this game are unusually local.

Myanmar’s online retail market is growing fast, expanding at roughly 13% a year through 2027 by DHL’s estimates. Tens of millions of people are now online, the overwhelming majority reaching the internet through a smartphone rather than a laptop. That single fact shapes everything: this is a mobile-first market, and any platform that is clunky on a phone is already losing.

Then there is the Facebook factor. In Myanmar, Facebook and Messenger are not just social networks; for a huge share of businesses they are the storefront, the catalogue, and the checkout counter all at once. Customers discover products in their feed, ask questions over Messenger, and place orders in a chat thread. This is why social listening, which means tracking what people say about brands on social media, is not a nice-to-have in Myanmar. It is often the clearest window you have into who is winning and why.

Finally, follow the money and the parcels. Cash-on-delivery is still king, closely followed by mobile wallets like KBZPay and Wave Money, because card penetration remains low. And delivery speed has become a bragging right, with the sharpest players promising same-day or even two-hour delivery in Yangon. Keep those three battlegrounds in mind, payments, delivery, and social, because they decide most of the fights below.

A note on the numbers: figures like market growth, internet penetration, and Facebook usage move quickly and vary by source. Treat the headline stats here as directional, and refresh them against a single current source before you rely on them for a decision.

Why one big exit changes the whole game

Shop.com.mm was not the only casualty. The fashion marketplace rgo47 also shut down, and it was not the first pivot the market has seen. Every closure does two things at once: it removes a competitor, and it releases a pool of customers and sellers who now need a new home.

For the survivors, this is opportunity and pressure in equal measure. Opportunity, because there is suddenly demand to capture. Pressure, because those newly homeless customers are shopping around, comparing, and perfectly willing to switch. In a shakeout, the brands that understand shifting sentiment fastest are the ones that convert a rival’s collapse into their own growth. Which brings us to the survivors.

The contenders, by category

Here is the full field, grouped by where each player actually competes.

Grocery and retail chains: the heavyweights

City Mall Online (City Mart). If Myanmar e-commerce has an incumbent champion, this is it. City Mart Holdings is the country’s largest supermarket group, and its online arm sells everything from groceries and baby care to beauty, home, and pet supplies. Its advantages are the boring, decisive ones: trust, scale, and logistics. It even uses its convenience-store brand, City Express, to sell quick-serve foods online, and it leans hard into fast delivery and cashless payments. Any challenger has to match a machine that has spent years earning shoppers’ confidence.

Capital Online (Capital Retail). Backed by the CDSG conglomerate, Capital runs Myanmar’s first modern-trade hypermarkets and brings that stability online, offering a broad mix of local and imported goods with home delivery and e-wallet payments. It is the credible number two in general merchandise: not the biggest, but well-funded and hard to dislodge.

Makro Click (Makro Myanmar). The odd one out, in a good way. Wholly owned by Thailand’s Siam Makro, Makro plays the business-to-business game, supplying restaurants, retailers, and institutions with bulk groceries through a membership model. Ordinary shoppers cannot really use it, and that is the point. Makro is not fighting for your weekly groceries; it is quietly owning the HORECA and trade-supply niche while everyone else scraps over consumers.

Electronics and tech: the two-horse race

ICT.com.mm. Branding itself the number-one online tech retailer in Myanmar, ICT sells smartphones, laptops, PCs, and accessories with the tactics tech buyers respond to: aggressive deals, click-and-collect, and buy-now-pay-later. Its app is well rated, and it competes on price and urgency.

Technoland. The seasoned veteran, founded in 2000, with a dozen stores across several cities and a deep catalogue spanning everything from student laptops to Apple gear to networking equipment. Its edge is physical presence and after-sales service, warranty, and on-site support, which matters enormously when someone is spending real money on a device.

UNiQUE.com.mm. The lifestyle-tech specialist, positioning itself around authentic, branded gadgets, from computers and phones to cameras and appliances. In a market where fakes are a genuine worry, UNiQUE’s whole pitch is trust in what you are buying.

The story here is a genuine rivalry: ICT competes on deals and speed, Technoland on service and range, UNiQUE on authenticity. Whoever a shopper believes on price and legitimacy wins the sale.

Fashion, beauty, and lifestyle: authenticity is everything

Sein Gay Har. Myanmar’s first department store, dating to 1985, now selling online across the same sprawling range as its shops, from groceries and clothes to electronics and furniture. Its weapon is legacy. Decades of high-street trust translate into online credibility that a startup simply cannot buy.

KhitZay. The challenger, chasing the fashion-and-lifestyle crowd with branded apparel, shoes, bags, and accessories, and staking its reputation on authenticity and easy returns. In a category where counterfeits and refund horror stories scare buyers off, “genuine products, easy returns” is a sharp positioning.

Medicare. A health-and-beauty specialist with roots in Vietnam and a growing Myanmar footprint, selling cosmetics, personal care, and wellness products both online and in-store. It competes on affordable, dependable everyday essentials.

Marketplaces and C2C: platforms, not shops

Zegobird. A broad online marketplace launched in 2017, bringing fashion, electronics, and home goods under one roof, a little like a compact local Amazon, with a mobile app and a promotions-and-reviews model.

365Myanmar. A general shopping portal that also lets third-party sellers list their own products, giving it a marketplace flavour and appeal to smaller retailers who want a ready-made shopfront.

iMyanmarMarket. The peer-to-peer heavyweight, effectively Myanmar’s online bazaar, where individuals buy and sell new and secondhand items, from phones to furniture to cars. Its strength is the sheer breadth of listings and its popularity for secondhand goods.

Remax. A focused single-brand store for mobile accessories, power banks, chargers, earbuds, and the like, run by the brand’s local distributor and leaning on frequent promotions and loyalty perks. Narrow, but well-defended within its niche.

How they actually compete

Strip away the category labels and almost every one of these players is fighting on the same three fronts.

Payments. Nearly all of them offer cash-on-delivery plus mobile wallets, because that is what customers trust. Card-on-checkout is growing but still not the default. If your payment flow does not include COD and wallets, you are excluding most of the market.

Delivery. Speed and reliability have become genuine differentiators, and app-based order tracking is fast becoming table stakes. City Mall Online’s two-hour Yangon delivery is the kind of promise that quietly wins repeat customers.

Social. This is the real arena. Because discovery, questions, and even sales happen on Facebook and Messenger, the brands that monitor social sentiment closely, catching complaints early, spotting what is resonating, and watching competitors’ buzz, get an information edge the others do not. This is precisely why serious competitor analysis in Myanmar has to include social listening, not just a look at each rival’s website.

What it all means: the competitor takeaways

Pulling the threads together:

The incumbents are hard to beat on trust. City Mart and Sein Gay Har convert decades of high-street credibility into online confidence. Challengers cannot out-trust them; they have to out-specialise them.

Niches are safer than open war. Makro (B2B) and Remax (accessories) thrive precisely because they are not fighting everyone at once. A well-defended niche beats a weak claim to the whole market.

In electronics, it is a real duel. ICT versus Technoland versus UNiQUE is decided on price, service, and authenticity. There is room for more than one winner, but not for a fourth generic clone.

In fashion, authenticity and returns are the whole ballgame. KhitZay’s bet on genuine products and easy returns is the right bet, because it targets buyers’ single biggest fear.

Marketplaces live or die on trust and usability. For Zegobird, 365Myanmar, and iMyanmarMarket, the battle is app experience, seller quality, and buyer confidence.

Across all of it, one thing is constant: the winners are the ones who understand their customers and their rivals better than the competition does. In a market with little reliable public data and a shakeout in progress, that understanding does not come from guessing. It comes from research.

Where this leaves you (and where MPR fits)

If you sell online in Myanmar, or you are thinking about entering, the exit of a major player is the moment to move, and the moment to make sure you are moving in the right direction. That means knowing where the freed-up customers are going, how sentiment is shifting on social, and where each competitor is strong and exposed.

That is the work we do. Magnify Plus Research runs market research, competitor analysis, and Burmese-language social listening across Myanmar and Asia, turning the noisy, fast-changing e-commerce landscape into a clear picture you can actually act on. If you want to know who is really winning your category, and why, that is a question we can answer with data rather than hunches.

Frequently asked questions

Who are the biggest e-commerce players in Myanmar in 2026? The leaders span several categories: City Mall Online (City Mart) and Capital Online in grocery and general retail, ICT.com.mm and Technoland in electronics, Sein Gay Har and KhitZay in fashion and lifestyle, and marketplaces like Zegobird, 365Myanmar, and iMyanmarMarket. Makro serves the B2B wholesale niche.

Why did Shop.com.mm close? The Alibaba-backed platform ceased operations in Myanmar in April 2026. Its exit, alongside the closure of the fashion site rgo47, has opened space for local players to capture displaced customers and sellers.

How do Myanmar shoppers pay and receive orders? Cash-on-delivery remains the most trusted method, followed by mobile wallets such as KBZPay and Wave Money. Card payments are growing but not dominant. Fast delivery and app-based order tracking are increasingly expected.

Why is social listening so important for e-commerce in Myanmar? Because Facebook and Messenger are where discovery, customer questions, and even sales happen. Monitoring social sentiment is often the clearest, fastest way to track brand health and competitor performance in this market.

Want to know who is winning your category? MPR runs competitor analysis, market research, and social listening across Myanmar and Asia.

Meta keywords

Sources: company websites and app stores (City Mall Online, Capital, Makro, ICT.com.mm, Technoland, UNiQUE, Sein Gay Har, KhitZay, Medicare, Zegobird, 365Myanmar, iMyanmarMarket, Remax), business profiles, and market reports including DHL e-commerce trends for Myanmar. Figures are directional and should be verified against a single current source before publication.

Myanmar’s small business landscape continues to evolve in response to an unstable business and economic environment. While inflation, currency depreciation, rising operating costs, foreign exchange challenges, and supply chain disruptions continue to pressure businesses, many small and medium-sized enterprises (SMEs) have demonstrated remarkable resilience by embracing digital technologies, mobile payments, social commerce, and innovative business models.

Looking ahead to 2027, businesses that prioritize operational efficiency, digital transformation, customer-centric strategies, and financial resilience are expected to be better positioned to capture emerging opportunities despite continued market uncertainty.

This article explores the most important small business trends shaping Myanmar in 2026 and 2027 and provides practical insights for entrepreneurs, business owners, and investors.

Myanmar’s Economic and Business Environment

Myanmar’s economy is showing gradual signs of stabilization, although businesses continue to operate in a challenging environment. According to international financial institutions, economic growth is expected to improve modestly in 2026 and 2027. However, inflation remains elevated due to currency depreciation, higher fuel prices, increasing logistics costs, and imported inflation.

Over the past several years, businesses have adapted to an evolving economic environment characterized by changing regulations, foreign exchange volatility, supply chain disruptions, and cautious consumer spending. As a result, many SMEs are prioritizing business continuity, operational efficiency, and sustainable growth instead of rapid expansion.

Although consumer spending remains constrained, demand continues to exist for businesses that provide value, affordability, convenience, and trusted products.

Trend 1: Social Commerce Continues to Dominate

Social commerce remains one of the strongest growth drivers for Myanmar’s SMEs.

Facebook continues to be the country’s largest digital marketplace, while TikTok has become an increasingly influential platform for product discovery, entertainment, and live selling. Messenger and Viber remain important communication channels for customer inquiries, order management, and after-sales support.

Consumers are increasingly comfortable purchasing products directly through social media without visiting traditional websites.

Businesses that consistently create engaging content, respond quickly to customer inquiries, and build strong online communities are gaining competitive advantages.

What businesses should do

Invest in high-quality short-form video content.

Build consistent brand presence across multiple social platforms.

Use live selling to increase customer engagement.

Strengthen customer service through messaging platforms.

Encourage user-generated content and customer reviews.

Trend 2: Mobile Payments Become Standard

Myanmar’s digital payment ecosystem continues to expand.

Mobile wallets and QR payment systems have become essential for businesses of all sizes. Customers increasingly expect cashless payment options that are fast, convenient, and secure.

Digital payments also improve operational efficiency by reducing cash handling, improving transaction records, and simplifying financial management.

Business opportunities

Faster payment collection

Better financial tracking

Improved customer convenience

Stronger customer loyalty

Businesses that have not yet adopted digital payment systems risk losing customers to more convenient competitors.

Trend 3: Customers Are Becoming More Price Sensitive

Inflation and rising living costs continue to influence purchasing behavior.

Consumers are spending more carefully and comparing prices before making purchasing decisions. Value for money has become one of the most important factors affecting purchase decisions.

Many customers now prioritize:

Essential products

Affordable alternatives

Promotions and discounts

Smaller package sizes

Trusted local brands

Businesses that clearly communicate value, quality, and affordability are more likely to retain customers.

Trend 4: Digital Marketing Is Becoming More Data Driven

Marketing based on intuition alone is becoming less effective.

Businesses are increasingly using customer insights, social listening, and digital analytics to understand consumer preferences, monitor competitors, and evaluate campaign performance.

Data-driven marketing enables businesses to:

Understand changing customer behavior.

Identify emerging market trends.

Measure marketing effectiveness.

Improve return on investment.

Make faster business decisions.

For SMEs with limited marketing budgets, investing in analytics often delivers greater long-term value than increasing advertising spend.

Trend 5: Artificial Intelligence Is Becoming More Accessible

Artificial Intelligence (AI) is no longer limited to large corporations.

Affordable AI-powered tools now help small businesses improve productivity, reduce costs, and automate repetitive tasks.

Common applications include:

Content creation

Customer service chatbots

Translation

Graphic design

Sales forecasting

Inventory management

Marketing automation

Rather than replacing employees, AI is increasingly supporting teams by improving efficiency and enabling staff to focus on higher-value work.

Trend 6: Local Brands Continue to Gain Consumer Trust

Consumers are increasingly supporting local businesses that offer reliable quality, competitive pricing, and strong customer service.

Many SMEs are successfully competing with imported products by:

Offering locally relevant products.

Responding quickly to customer feedback.

Building authentic brand identities.

Providing personalized customer experiences.

Businesses that invest in brand trust and long-term customer relationships are expected to outperform competitors focused solely on pricing.

Trend 7: Diversified Sales Channels Improve Business Resilience

Businesses are reducing dependence on a single sales channel.

Successful SMEs now combine:

Physical retail stores

Facebook Shops

TikTok Shop

Messaging applications

Online marketplaces

Wholesale partnerships

A diversified sales strategy helps businesses manage demand fluctuations and reach different customer segments.

Trend 8: Operational Efficiency Becomes a Competitive Advantage

Rising operating costs are encouraging businesses to improve efficiency.

SMEs are investing in:

Inventory management systems

Digital accounting

Customer relationship management (CRM)

Process automation

Staff training

Better financial planning

Businesses that effectively control costs while maintaining product quality are better positioned to remain competitive.

Trend 9: Sustainability Is Becoming a Business Opportunity

Consumers are becoming more aware of environmental responsibility.

Although sustainability remains an emerging trend in Myanmar, many businesses are beginning to adopt practices such as:

Eco-friendly packaging

Reduced plastic usage

Energy-efficient operations

Waste reduction

Responsible sourcing

These initiatives not only strengthen brand reputation but can also reduce long-term operating costs.

Trend 10: Customer Experience Is a Key Differentiator

Products alone are no longer enough to build customer loyalty.

Customers increasingly value:

Fast response times

Reliable delivery

Clear communication

Personalized service

Easy purchasing experiences

Consistent product quality

Businesses that consistently deliver positive customer experiences generate stronger repeat purchases and word-of-mouth referrals.

Key Challenges Facing Myanmar SMEs

Despite positive opportunities, businesses continue to face several challenges:

Inflation and rising operating costs

Foreign exchange volatility

Supply chain disruptions

Logistics and transportation challenges

Changing regulatory requirements

Limited access to financing

Increasing digital competition

Skilled workforce shortages

Global economic uncertainty

Businesses that proactively plan for these risks will be more resilient over the long term.

Opportunities for Growth in 2027

Several sectors are expected to offer promising opportunities, including:

Digital services

E-commerce and social commerce

Food and beverage

Health and wellness

Education and online learning

Tourism and hospitality

Agriculture and agribusiness

Financial technology

Renewable energy solutions

Business consulting and professional services

Companies that combine innovation with operational discipline are likely to benefit from these emerging opportunities.

Recommendations for Small Business Owners

To remain competitive in 2027, SMEs should consider the following priorities:

Strengthen digital marketing capabilities.

Adopt data-driven decision making.

Expand digital payment options.

Diversify sales channels.

Invest in customer experience.

Improve operational efficiency.

Explore practical AI applications.

Build financial resilience through careful cash flow management.

Strengthen supplier relationships.

Continuously monitor changing consumer behavior.

Conclusion

Myanmar’s small business sector has demonstrated remarkable adaptability despite operating in a challenging business environment. Businesses that continue investing in digital transformation, customer experience, operational efficiency, financial resilience, and sustainable growth strategies are expected to be best positioned for long-term success.

While market conditions remain uncertain, innovation, agility, and data-driven decision making will continue to shape the next phase of SME growth in Myanmar. SMEs that embrace these trends today will be better equipped to navigate future challenges and seize new opportunities in 2027 and beyond.

About Magnify Plus Research

Magnify Plus Research provides market research, consumer insights, social listening, and strategic intelligence to help organizations make informed business decisions. By combining advanced analytics with local market expertise, we empower businesses to understand changing consumer behavior, identify emerging trends, and uncover new opportunities for sustainable growth in Myanmar.

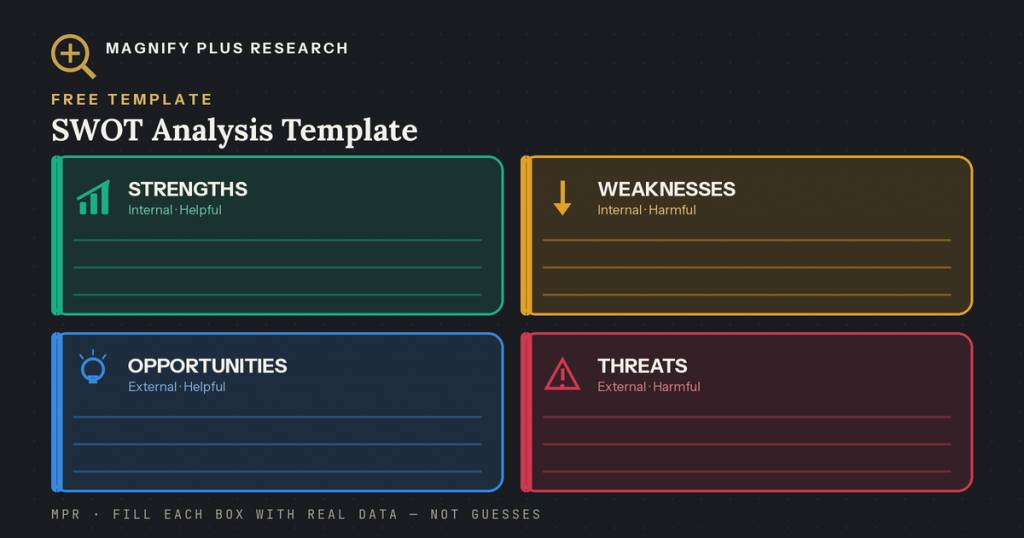

Your competitors in Myanmar aren’t standing still, and in a market this fast and this hard to read, the businesses that win are usually the ones that understand their own position most honestly. A SWOT analysis is the simplest, most durable tool for doing exactly that. It forces four uncomfortable, useful questions: what are we good at, where are we weak, what could we seize, and what could hurt us?

This guide shows you how to run a SWOT analysis and turn it into real competitor analysis in Myanmar, with a free template, worked examples relevant to Myanmar and the wider Asia market, and the one thing most SWOT guides skip: how to fill it with real data instead of guesswork.

What is a SWOT analysis?

A SWOT analysis is a simple framework that maps your business across four categories: Strengths, Weaknesses, Opportunities, and Threats. These are usually laid out as a two-by-two grid, and the magic is in how those four boxes are split along two axes:

Internal vs. external. Strengths and weaknesses are internal, things inside your control (your team, your product, your pricing). Opportunities and threats are external, forces in the market you don’t control (competitors, regulation, consumer shifts).

Helpful vs. harmful. Strengths and opportunities help you; weaknesses and threats harm you.

Put those together and you get the classic matrix: internal-helpful (Strengths), internal-harmful (Weaknesses), external-helpful (Opportunities), external-harmful (Threats).

Why SWOT matters for businesses in Myanmar and Asia

SWOT is useful everywhere, but it earns its keep in Myanmar and across Asia for specific reasons:

The market moves fast. Inflation, shifting consumer behaviour, new digital platforms, and a volatile operating context mean a position that was strong last year may be exposed today. SWOT gives you a regular, structured checkpoint.

Reliable data is scarce. In many Asian markets, and Myanmar especially, you can’t just download a competitive report and call it insight. A SWOT forces you to ask what you actually know versus what you’re assuming, which is exactly the discipline a low-data market demands.

Competition is intense and local. The players who win in Myanmar are often strong local and regional brands, not the international names you’d expect. A SWOT anchored in real market research in Myanmar keeps you honest about who you’re really up against.

Done well, a SWOT helps you play to your strengths, fix your weaknesses before they cost you, move on opportunities before rivals do, and see threats coming while you can still respond.

The four components, with Myanmar examples

Strengths (internal · helpful)

Strengths are the internal advantages you can build on, the things you do better than rivals. In a Myanmar context, real strengths might include a trusted local brand name, a strong distribution network into secondary cities, a genuine understanding of Burmese-language consumers, or an established presence on Facebook and Messenger where commerce actually happens.

Weaknesses (internal · harmful)

Weaknesses are the internal gaps that hold you back. Common ones here: over-reliance on a single city (usually Yangon), thin data on rural consumers, a cash-only payment flow in a market moving to mobile wallets, or a product priced for a pre-inflation consumer.

Opportunities (external · helpful)

Opportunities are external shifts you can ride. Think: the rapid growth of mobile money, the rise of social commerce, a young and phone-native population, or a competitor stumbling in a category you could own. (Our Myanmar consumer trends overview is a good source of these.)

Threats (external · harmful)

Threats are external forces that could damage you: aggressive local competitors, regulatory or currency shifts, supply-chain and power disruptions, or changing consumer priorities under economic pressure. Naming them doesn’t make them go away, but it lets you plan.

From SWOT to competitor analysis in Myanmar

A SWOT of your own business is step one. Competitor analysis is where it gets powerful: you run a SWOT on each major rival too, then compare. That comparison reveals the gaps: the opportunities they’re ignoring, the weaknesses you can exploit, the strengths you need to neutralise.

In Myanmar, the hard part isn’t the framework; it’s the inputs. Competitor analysis is only as good as the intelligence behind it, and in a market with little public data, that intelligence has to be gathered deliberately: through consumer research, social listening, retail and channel checks, pricing audits, and on-the-ground fieldwork. A SWOT grid filled with assumptions is just a tidy-looking guess. A SWOT grid filled with real data is a strategy.

The examples below are illustrative archetypes, not profiles of specific companies. They show what a realistic SWOT looks like in this region.

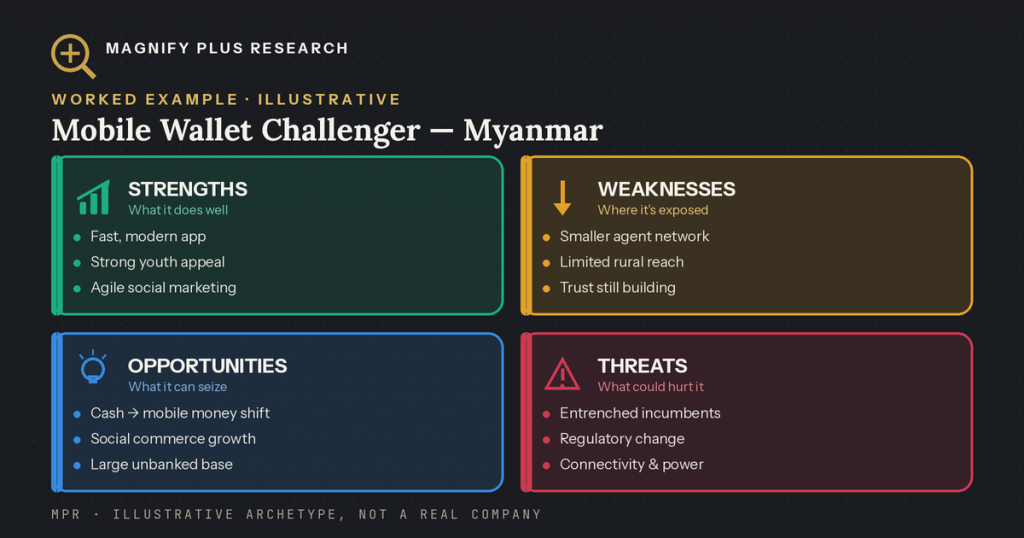

Example 1: A mobile wallet challenger (Myanmar)

Strengths: fast, modern app; strong appeal to young urban users; agile marketing on social platforms.

Weaknesses: smaller agent network than incumbents; limited reach in rural areas; brand still building trust for a financial product.

Opportunities: rapid shift from cash to mobile money; growth of social commerce needing embedded payments; a large unbanked population.

Threats: entrenched incumbents with bigger networks; regulatory change; connectivity and power reliability; consumer caution about digital finance.

Example 2: An FMCG brand entering Myanmar

Strengths: established regional supply chain; strong product quality; capital to invest.

Weaknesses: no local brand recognition; distribution built for other markets; limited grasp of Burmese consumer nuance.

Opportunities: “premium-affordable” positioning as consumers seek value; under-served categories; social-first route to market.

Threats: strong incumbent local brands; price sensitivity under inflation; the cost and difficulty of national distribution.

Example 3: A regional e-commerce player expanding across Asia

Strengths: proven platform and logistics tech; scale and brand across multiple markets.

Weaknesses: one-size-fits-all playbook that ignores local behaviour; thin last-mile coverage in newer markets.

Opportunities: rising smartphone penetration across Asian markets; demand for reliable online retail; partnerships with local sellers.

Threats: hyper-local competitors; varied regulation across borders; logistics and payment fragmentation.

How to do a SWOT and competitor analysis in Myanmar, step by step

Define the objective and the competitive set. What decision is this for? Who are the two or three rivals that actually matter? A vague SWOT of “the market” helps no one.