Here is a fact about Myanmar e-commerce that breaks regional brand teams’ brains.

The country has somewhere between four and five billion US dollars of online shopping activity. It has 19 million people walking around with an active KBZPay wallet in their pocket. And the single most important e-commerce platform in the country, by a long margin, is not a marketplace app. It is a Facebook page. With a person on Messenger. Who takes cash on delivery.

If you came to this article from a regional dashboard expecting a Lazada and Shopee story, take a breath. Myanmar is doing its own thing. The major regional marketplace that did try, Shop.com.mm, the Daraz backed platform, has exited the market. The other early formal player, rgo47, has faded out of relevance. What is left of the formal marketplace layer is a small set of names that real Myanmar shoppers actually use, and a much larger informal layer that almost no regional dashboard captures.

This is a field report from where we sit, between Yangon and Mandalay, watching the carts fill up. Sources for every figure are at the bottom. Pour a coffee.

How Big, How Fast

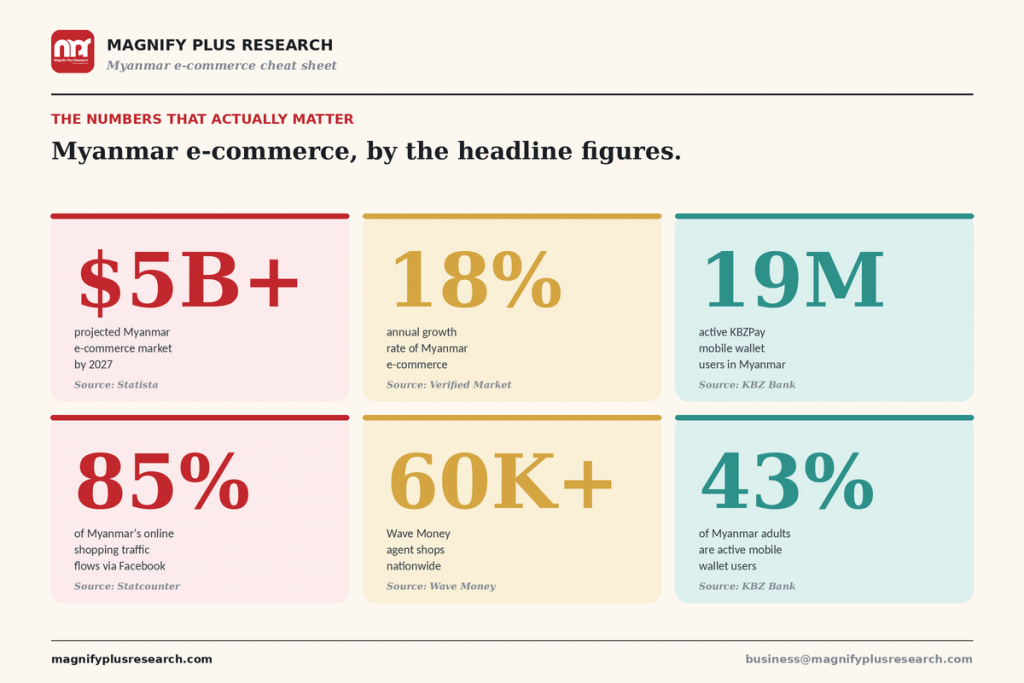

Start with the size. Different research houses count Myanmar’s online economy differently, but the consensus shape is the same. The Myanmar e-commerce market is projected to reach a valuation of approximately 4.5 billion US dollars by the end of 2025, growing at an annual rate of over 18%. Statista’s longer view pegs the eCommerce market in Myanmar to grow by 13.21% (2023 to 2027), resulting in a market volume of US 5.14 billion by 2027. The wider digital commerce category, including digital services, is projected to grow by 25.75% (2024 to 2029) resulting in a market volume of US 5.66 billion in 2029.

Translate the numbers. Myanmar online shopping is roughly doubling on a five year view, in a country where official GDP has been wrestling with currency volatility, inflation, and supply chain frictions the whole way through. That is not a small thing. Consumers are choosing to buy online faster than the macro environment would predict. That is a behavior shift worth paying attention to.

Two reasons it is happening, both at the same time.

One, the phones are everywhere. Myanmar is mobile first to a degree that still surprises foreign visitors. Browsing, comparing, paying, and conversing with sellers all happen on a phone screen. The desktop e-commerce experience, in the way it exists in Singapore or Bangkok, barely exists here.

Two, the wallets caught up to the phones. The number of active KBZPay users jumped by four million in 2024, to reach 19 million in total across Myanmar, representing 43% of the adult population. Add Wave Money on top of that, with over 60,000 Wave Shops nationwide and the Wave App as its dedicated mobile wallet, and you have the two giants moving most of the digital money. CB Pay and AYA Pay, the bank backed wallets, are pushing aggressively for share in 2026. Half the adult population is moving money digitally, every day, on rails that did not really exist a decade ago. E-commerce was waiting for this. The wallets unlocked it.

And then in 2025 the Central Bank of Myanmar dropped MMQR, the national QR code payment standard. Suddenly any wallet could pay any merchant through a single, standardized QR. That is a quiet, profound piece of infrastructure. It means the consumer no longer has to care which wallet the seller accepts. They scan the same code with whatever app they have. For e-commerce, that removes one of the last meaningful friction points at checkout.

The Plot Twist: This Whole Thing Runs on Facebook

The thing regional templates get most wrong about Myanmar is the channel mix.

In Indonesia, you talk about Shopee and Tokopedia. In Thailand, Lazada and Shopee. In Vietnam, Shopee and TikTok Shop. In Myanmar, you have to talk about Facebook first, Messenger second, and the marketplace apps a distant third. In fact, Facebook is one of the main platforms people use to sell their products, as it takes up 85% of online traffic per a statcounter study.

Walk this through. A consumer in Mandalay sees a product on a Facebook page. She messages the seller in Burmese. They negotiate price and delivery. She pays cash to a courier when the parcel arrives, or scans an MMQR code with whichever wallet she has if she trusts the seller. None of this transaction touches a marketplace platform’s shopping cart. None of it gets counted in the way Statista counts e-commerce in Jakarta. It still happens, millions of times a month, and it is the dominant model by a long way.

The implication for brands is direct. If your Myanmar e-commerce plan starts with a Lazada style fulfillment integration and ends with a programmatic ads buy, you are optimizing for a channel that does not really exist here. Building a Myanmar e-commerce strategy without a serious social commerce play is like opening a Bangkok restaurant without Line or a Jakarta one without WhatsApp. Technically possible. Strategically odd.

Where Myanmar Actually Shops

Here is the playing field, in plain language.

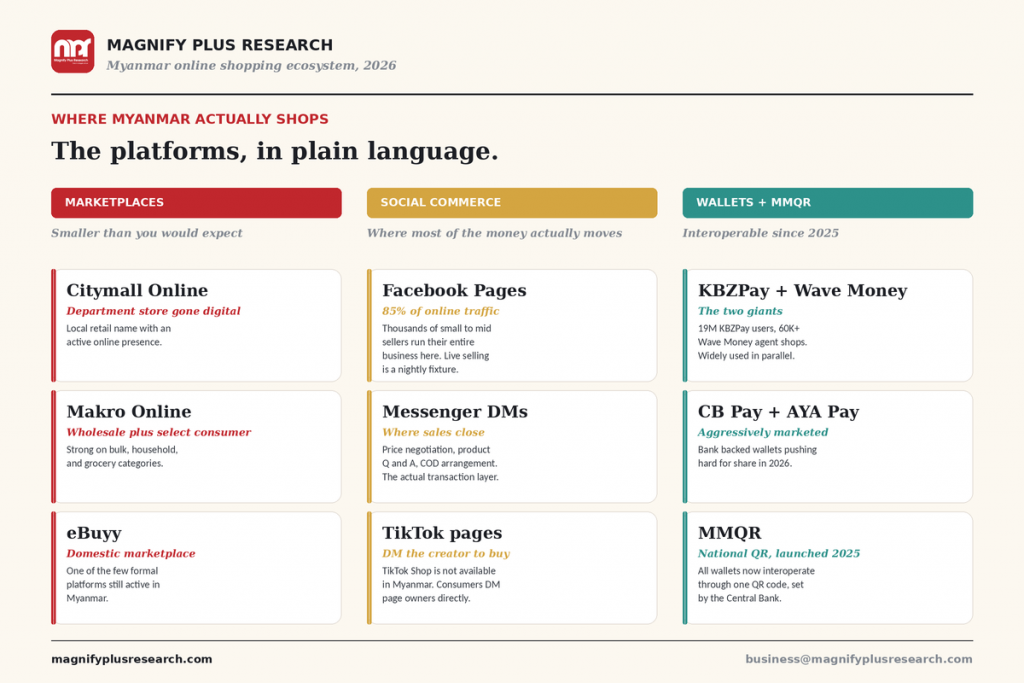

The formal marketplaces (smaller than you would expect). The list of formal marketplaces actively used by Myanmar consumers in 2026 is short. Citymall Online runs the digital arm of a recognized local department store. Makro Online serves bulk, household, and grocery categories. eBuyy is one of the few remaining domestic marketplace platforms with active traffic. That is roughly the picture. Shop.com.mm has exited Myanmar, rgo47 has lost relevance, and TikTok Shop is not available in this market. The clean formal marketplace experience that exists across the rest of the region simply has not consolidated here.

The social commerce layer (where most of the money moves). Facebook pages, Messenger DMs, and TikTok creator pages, with DMs as the actual transaction layer. A Myanmar brand without a social commerce operation is leaving most of the addressable e-commerce market on the table. A foreign brand without a social commerce partner is, depending on category, leaving an even bigger share. Important detail on TikTok, since the regional template gets this wrong: TikTok Shop is not live in Myanmar. Consumers discover products on creator pages and TikTok lives, then DM the page owner to buy. The actual purchase happens the same way Facebook commerce does, in a chat thread, with COD or a wallet payment at the end.

The wallets and MMQR. KBZPay and Wave Money are the two giants, with 19 million active KBZPay users and 60,000 plus Wave Money agent shops nationwide. They are used in parallel by most consumers. CB Pay and AYA Pay are the bank backed wallets being aggressively marketed in 2026. And sitting on top of all of them, MMQR, the national QR payment system launched in 2025 by the Central Bank, makes every wallet interoperate. One QR, any wallet, any merchant. For e-commerce this is the unlock the market has been waiting for.

Last mile. Foodpanda still operates in food, with a long tail of local couriers, motorbike networks, and bus express services handling parcels. Last mile remains the weakest part of the experience, which is also where the differentiation is for any brand willing to invest.

What Categories Are Winning

Different shapes of online demand are emerging across categories in Myanmar, and a few patterns are clear enough to call out.

Mobile and electronics. The category that grew up online first in Myanmar, and still the comfort zone for high ticket online shopping. Consumers compare specs and prices across multiple Facebook sellers before deciding. Brand and seller trust both matter.

Fashion and beauty. Heavily social, heavily live. Live selling sessions on Facebook Live for Burmese audiences are now a routine evening fixture. TikTok creator pages are increasingly important for product discovery, with the actual sale happening in DM. Influencer driven product launches in fashion and beauty regularly outperform traditional retail launches in reach, if not yet in conversion.

Groceries and FMCG. Slower to migrate online for habitual purchases, but accelerating. Makro Online has taken a share of the bulk and household category. The grocery story is partly a city story (Yangon ahead, Mandalay catching up, rural townships still firmly traditional trade) and partly a logistics story.

Home and appliances. A surprising bright spot. Consumers willing to commit to higher ticket online purchases when the brand and seller credibility line up, and when COD or an installment option is on the table.

Buy Now Pay Later style options. Still nascent in Myanmar relative to the rest of the region, but the conditions for it are in place. The brand or fintech that gets this right will unlock a meaningful slug of higher ticket online demand.

What Works and What Does Not

A few observations from the field, blunt edition.

Cash on delivery still rules. It is not the future. It is the present. Brands that try to force prepaid only checkout flows on Myanmar consumers, often because their regional template assumes a different trust environment, leave conversion on the floor. Build for COD as the primary path. Treat digital prepay as the upgrade, helped along by the MMQR interoperability.

Delivery promises kept beat delivery promises made. Overpromising delivery windows is the single most common consumer complaint in Myanmar online shopping, and it shows up in our social listening every week. Quiet, reliable, twice as long as you would brag about is better than fast, public, and frequently late.

Live selling beats static product pages. A Facebook Live with a seller talking through a product in Burmese, taking questions in real time, and dropping a price for the next ten minutes, outsells a polished static product card by margins that surprise regional brand teams every time we share the data. Live is not a tactic in Myanmar. It is a channel.

Burmese language descriptions matter more than you think. Product titles, descriptions, and customer service in Burmese convert dramatically better than the same content in English. Even on platforms where consumers can read both, Burmese signals trust and seriousness. English signals “I do not really care about you.”

Returns are the trust battleground. Myanmar consumers have learned to be cautious about online quality because they were burned in the early years of formal e-commerce. Generous, visible, fast return policies disproportionately reward the brands that offer them.

The Influencer and Live Commerce Boom

Live commerce, the blend of live streaming and instant purchase that took China by storm, has quietly become a big deal in Myanmar over the last two years. The format suits the market structurally. Burmese consumers like to ask questions before buying, like to see a product demonstrated by a real person, and like the social proof of watching other viewers buy in real time. Live selling delivers all three.

The interesting variant is that Myanmar live commerce is less centralized than China or Thailand. It is not dominated by a handful of mega influencers on a single platform. It is a wide layer of small to mid scale sellers running their own Facebook Live sessions, three to five nights a week, with audiences of a few hundred to a few thousand each. TikTok creators run a similar playbook on their own pages, with the buy happening in DM rather than through a built in shop button. The aggregate is enormous. The visibility, for foreign brand teams looking at platform dashboards, is low.

Which is exactly the kind of asymmetry that makes Myanmar market research valuable. The signal is there. You just have to look at it through Burmese eyes.

Why This Should Matter to Your Brand Plan

A few practical takeaways.

For foreign brands considering Myanmar, accept that the channel mix you planned for is probably wrong. A Myanmar e-commerce play should over index on social commerce, Facebook Live capability, Messenger conversational sales, TikTok creator partnerships with DM driven conversion, and reliable COD logistics. Marketplace presence is optional. Social commerce capability is not.

For Myanmar brand owners, the structural advantage is on your side. You speak Burmese. You can run live sessions in language. Your team is one Messenger thread away from any consumer in the country. Most of the unsolved problems in Myanmar e-commerce, returns, delivery reliability, trust at the high ticket end, are problems where a smart local brand outperforms a heavyweight foreign one every time.

For investors and consulting firms watching the market, the data you need probably does not exist yet in a form you can buy off a regional dashboard. It exists in the fieldwork that captures actual Burmese consumer behavior, the social listening that surfaces the unprompted conversation in Burmese, and the channel mapping that follows real money through real platforms. Which is the kind of market research in Myanmar that MPR exists to do.

How MPR Helps

We are Magnify Plus Research, the market research arm of the Magnify Group, based in Yangon. We field consumer studies across Myanmar, run brand health and category tracking, and integrate with Magnify Group social listening built on Burmese language natural language processing. We work with foreign entrants, regional consulting firms, Myanmar brand owners, and investors.

If you are figuring out an e-commerce or category play in Myanmar and want fieldwork, sizing, or social signal that actually reflects how Burmese consumers behave, we should talk.

Get in touch: business@magnifyplusresearch.com

Frequently Asked Questions

How big is Myanmar’s e-commerce market in 2026? Estimates from Verified Market Research put the market at around 4.5 billion US dollars by end of 2025, growing 18% annually. Statista forecasts roughly 5.14 billion by 2027 and 5.66 billion in digital commerce overall by 2029.

What is the most popular online shopping platform in Myanmar? By transaction volume, it is not a platform in the formal sense. Around 85% of online shopping traffic flows through Facebook, with the actual sale closing in Messenger. Among the formal marketplaces still active in Myanmar, Citymall Online, Makro Online, and eBuyy are the names that get used. Shop.com.mm has exited the market and rgo47 has lost relevance.

Is TikTok Shop available in Myanmar? No. TikTok Shop is not live in Myanmar. Myanmar consumers use TikTok as a discovery and live selling channel, then DM the creator or page owner directly to arrange the purchase, much like Facebook commerce.

What payment methods do Myanmar online shoppers use? Cash on delivery is still the dominant payment method. KBZPay (around 19 million active users) and Wave Money (over 60,000 agent shops) are the leading mobile wallets and are widely used in parallel. CB Pay and AYA Pay, the bank backed wallets, are being aggressively marketed in 2026. MMQR, the national QR code system launched in 2025 by the Central Bank, now lets any wallet pay any MMQR enabled merchant through one standardized code.

Is Myanmar e-commerce mobile first? Yes, decisively. Browsing, purchasing, paying, and customer conversations all happen on mobile. Desktop e-commerce in Myanmar barely exists at scale.

What sectors are growing fastest in Myanmar online shopping? Mobile and electronics, fashion and beauty (heavily via live selling on Facebook and TikTok pages), home and appliances, and increasingly groceries and household via Makro Online and social sellers in urban centers.

Does live commerce work in Myanmar? Yes, especially Facebook Live and TikTok creator lives. Myanmar live commerce is less dominated by mega influencers than China or Thailand, with a wide base of small to mid scale sellers running regular live sessions in Burmese. The purchase typically happens in a DM thread after the live.

How can I research the Myanmar e-commerce market reliably? Through primary fieldwork in Burmese, social listening with Burmese natural language processing, and channel mapping that captures both the small formal marketplace layer and the much larger informal social commerce layer. Magnify Plus Research designs research programmes around exactly these questions. Reach us at business@magnifyplusresearch.com.

About the author: [BYLINE PLACEHOLDER, Name, role, credential line, headshot, LinkedIn.]

Get started: Want a sharper view of Myanmar’s e-commerce opportunity for your category? Email business@magnifyplusresearch.com.

Sources, DataReportal Digital 2026 Myanmar, Verified Market Research Myanmar ICT Market, Statista Myanmar eCommerce, 6Wresearch Myanmar E-commerce Market, FinanceAsia KBZ Bank 2025, Wave Money Myanmar, Central Bank of Myanmar MyanmarPay, Statcounter Myanmar traffic data, MPR field intelligence.